Illegal Insurance Certificate Requests Happen all the Time – One of the Industry’s Worst Kept Secrets:

Illegal Insurance Certificate Requests; Ladies and Gentlemen, If it’s not in the policy, we as brokers cannot — by law — put it on the certificate. Not for a GC; Not for a property manager; Not for an owner; Not for a lender. Not for “my legal department insists.”; And no, not even for a governmental authority with a fancy letterhead.

Yet every hour, brokers are asked to create coverage via certificates as if certificates were endorsement vending machines.

Spoiler: Magic is not covered by ISO.

The Law (Yes, It Actually Exists), Under NYS Insurance Law §§ 501–502, it is illegal to: “…add terms, conditions, warranties, guarantees, or language not expressly included in the policy…” and illegal for any party to: “…willfully require such language as a condition of work, payment, or contract…” Much of the language being requested on certificates describes legal concepts—not coverage that actually exists in the policy.

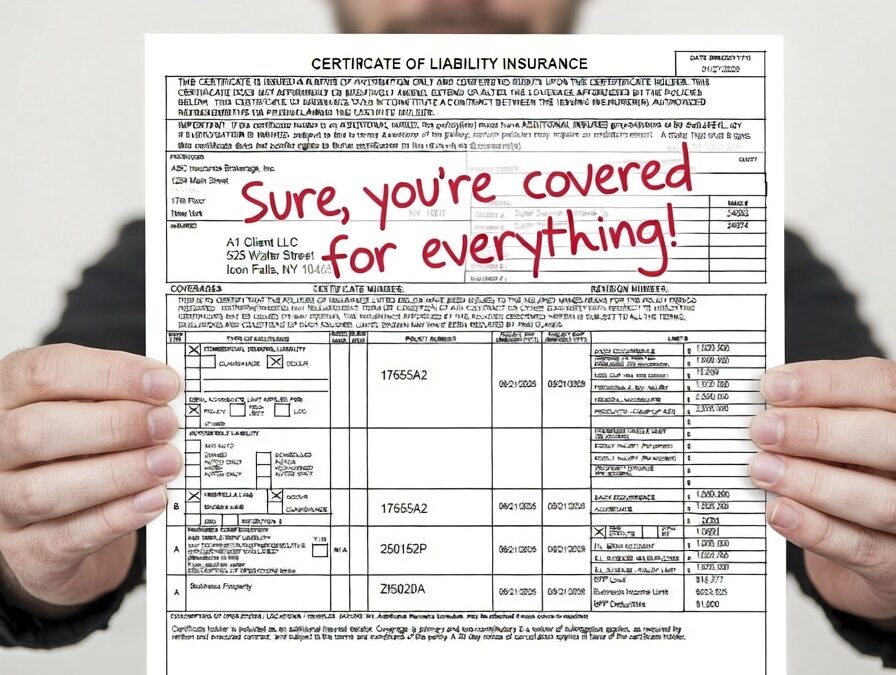

Translation: Certificates are evidence of insurance, not post-loss fan fiction.

The top of every certificate STATES:

THIS CERTIFICATE DOES NOT AMEND, EXTEND OR ALTER THE COVERAGE…

THIS CERTIFICATE DOES NOT CONSTITUTE A CONTRACT…

The Fine, yes there is a fine, NYS DFS enforces this: $1,000 first violation + $2,000 each subsequent (§503).

I served on the committee that enacted this law in 2015. The intent was clear:

- Certificates ≠ mini-contracts

- Certificates ≠ endorsements

MYTHS Brokers Hear Constantly

- “Just put it on the cert — we’ve always done it that way.”

- “Legal says the cert must say X.”

- “Add Third Party Action Over to the cert.”

- “We need the contractual liability to cover the contract.”

- “We won’t pay you until you issue the cert.”

- “GCs need it for risk transfer.”

FACTS (a.k.a. Reality + Law)

- Policies dictate coverage

- Legal should read §502 before mandating creative writing.

- If it’s not in the policy, it’s not going on the certificate.

- The policy is the contract; the certificate is the receipt.

The Real Point

Brokers/Agents aren’t trying to be ‘difficult’ we are:

- Protecting clients

- Protecting carriers

- Avoiding penalties

- Preventing coverage misunderstandings

If the issue is risk transfer, indemnity, or additional insured status, solve it in the contract or the policy — not through illegal COI demands.

Final Thought on Illegal Insurance Certificate Requests

- Insurance has enough complexities.

- We don’t need to invent new ones through certificate myth-making.

- Stop requesting brokers and agents to do illegal things.

- Start asking how to solve the actual coverage problem.

- Happy to talk to brokers, clients, GCs, PMs, owners, or authorities who want to understand this — ideally without a DFS citation.

Disclaimer: This article is provided for general informational and educational purposes only and does not constitute legal advice or an interpretation of any insurance policy.